- 13 Jun, 2024

- 0 Comments

- 6 Mins Read

🧠 This might be TOO controversial…

Welcome to reThinkable – my weekly newsletter where I share actionable insights to build a wealthy healthy life.

Here’s what we’re covering:

⚖️ Don’t focus on your investments

💸 How to increase your SR

Hey {{ name | reThinker }},

Before we dive into today’s email, I wanted to give you a quick heads up: there’s an update on the secret project I’ve been working on for the past few months somewhere in this newsletter.

Keep on reading and you’ll see it — it’s pretty exciting stuff.

Today, I want to talk about why you shouldn’t focus on your investment returns if you want to build wealth. Instead, you should focus on this thing called “SR.” I know — it’s controversial, but it’s going to make total sense.

⚖️ Don’t focus on your investments

For most things in life, the harder you work, the better the outcome.

But when it comes to investing, it’s the complete opposite.

Chances are, the harder you try to be a “good investor” and “optimize” your investment portfolio, the worse your returns will be.

Even long-term index fund investors will experience turbulent periods. For instance:

1990 to 1999 was one of the best 10-year periods for stock market performance. If you invested $10k in the S&P 500 at the beginning of each year, you would have approximately $280k by the end of 1999.

2000 to 2009, on the other hand, was one of the worst 10-year periods for stock market performance. If you applied the same strategy as the previous decade, you would have around $92k by the end of 2009.

Investment returns can vary quite a bit, even with 10-year long investing horizons.

To be clear, I’m not saying investing doesn’t matter when it comes to building wealth because it definitely does. Compound interest will make you wealthy in the long run.

However, in the short run, your Savings Rate (SR) has a much larger impact. Your Savings Rate is the percentage of your take-home pay that you save.

Consider 2 Scenarios:

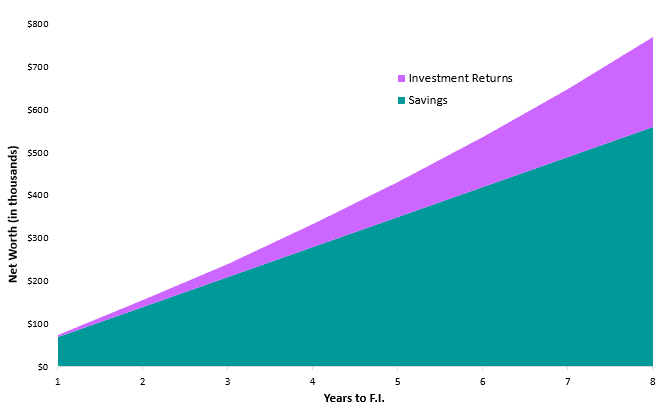

Scenario A: Sam earns $100k a year, has a 70% savings rate, and gets a 7% average annual return in the stock market. It would take Sam just about 8 years to reach financial independence. At this point, 73% of her total net worth came from her savings.

Zach – FPF

Scenario B: Josh also earns $100k, but has a 20% savings rate, and gets the same 7% average annual return in the stock market. In this scenario, it would take Josh about 30 years (nearly 4x longer) to reach financial independence. At this point, 71% of his total net worth came from his investments.

Zach – FPF

In both scenarios, Sam and Josh’s net worth was mostly from their savings in the beginning. But over time, Josh’s investments made up a larger portion of his net worth.

So basically, if you’re in the early to mid-stages of your financial journey, your Savings Rate (SR) will have more influence on your overall wealth than your investment returns.

💸 How to increase your SR

Increasing your Savings Rate boils down to 2 main financial levers: Income and Spending. Here are 3 ways you can pull on them.

1. Pull On Your Income

Increasing your income means you either need to start a side hustle or get a raise. I talked about my favorite strategy to get a raise in this newsletter issue already so I’ll focus on side hustles today.

When it comes to choosing a side hustle to start, the best tip I received is to play to your strengths, skills, and natural advantages. For example, I’m good at making videos, cooking, and finance. It doesn’t mean I’m the best at any of these three skills, but I know more than the average person.

If I chose to leverage my cooking skills, I could host cooking classes in my apartment and charge $90 to $150 per person, which is the going rate in NYC on Airbnb Experiences. Even if only 5 people sign up for my weekly classes, I could make an extra $1,800 to $3,000 a month.

If you want to start a side hustle, figure out what you’re better at than the average person. Then think about how you can monetize your talent. Are you good at soccer? Math? Drawing? Can you tutor others? Can you play competitively? Could you host a class?

2. Automate Your Money

Cutting your spending will increase your Savings Rate, but it’s tough for most people to consistently reduce their spending.

The problem is, people believe that personal finance is all about willpower. The idea goes like this: “if I just try harder, I’ll stop spending so much money,” but willpower rarely works.

After helping countless people with their finances, I realized the most effective way for people to manage their money was with financial automations. It’s something I’ve been doing for years, and it’s what allowed me to finally take control of my money, instead of it controlling me.

Basically, all my finances are taken care of without me needing to do anything. I don’t need to worry about whether I’m spending too much money, saving too little, or not investing enough because I’ve set up systems in place where everything happens on autopilot.

If financial automations sound interesting to you, I’m hosting a free 5-day Challenge starting on July 1st where I’ll teach you, step-by-step, how to automate your finances. It’s completely free, but space is very limited. I’ll share more details in the coming days.

3. Increase Your Savings Income

Yes, that cross-out was on purpose 😉. If you don’t want to ask for a raise or start a side hustle to increase your income, there is one other way to increase your income. It’s one of the very first things I did when I got into personal finance, and it’s something that continues to generate me income every month, without any effort on my part.

It’s opening a High Yield Savings Account (HYSA). It’s basically a savings account that pays you money. You might not realize it, but the amount you get paid to keep your savings in one is quite substantial.

Most HYSAs, like Laurel Road, UFB Direct, and Bask Bank, offer more than a 5% interest rate. Meaning, if you deposit $10,000 in a HYSA at a 5% interest rate, you earn $500 at the end of the year. This is compared to if you use Chase which offers a 0.01% interest rate. With Chase, you’d earn $1 at the end of the year.

If you’re interested in opening a HYSA, here are my favorite FDIC-insured ones where you can earn between more than 5% on your money.

P.S. If you need help setting up a HYSA, I created a free 2-minute video tutorial for y’all.

🔎 reThink More

⛽ US gas prices will continue dropping unless THIS happens.

📉 Here’s where rent is falling and where rent is increasing. Do you live here?

💰 Apparently earning $100k a year in the US isn’t enough to make you feel rich anymore. Here’s how much some think you need.

📝 reThinkable Quiz

P.S. Here’s the bear falling from a tree

If you enjoyed today’s newsletter, share it with your friends and family!

Was this forwarded to you? Sign up here.